- Hurricane Debby came ashore in South Carolina near Bulls Bay in August 2024 as a tropical storm, after first making landfall as a Category 1 hurricane in Florida. Its slow track stalled historic rainfall over Charleston and the Lowcountry, with river flooding inland in the Pee Dee and tornadoes in places like Edisto Beach.

- Because much of Debby's damage came from water, the central coverage question on these claims is often wind-versus-flood: wind and wind-driven rain are generally covered under a homeowners policy, while rising water, storm surge, and flooding are generally excluded and covered only under separate flood insurance.

- Contested SC Debby claims commonly turn on that wind-versus-flood line, on the application of a percentage hurricane or named-storm deductible, on roof scope and depreciation, and on matching where only part of a roof or structure is repaired.

- When a carrier refuses to pay a covered claim without reasonable cause, S.C. Code § 38-59-40 may allow a court to award attorney's fees — capped at one-third of the judgment — on top of the policy benefit, with the common-law bad-faith framework potentially adding more when conduct supports it.

- At Property People Law, we review SC Hurricane Debby claims and any denial at no cost. Our SC residential and commercial property work is generally on contingency — we only get paid from the recovery, not your pocket.

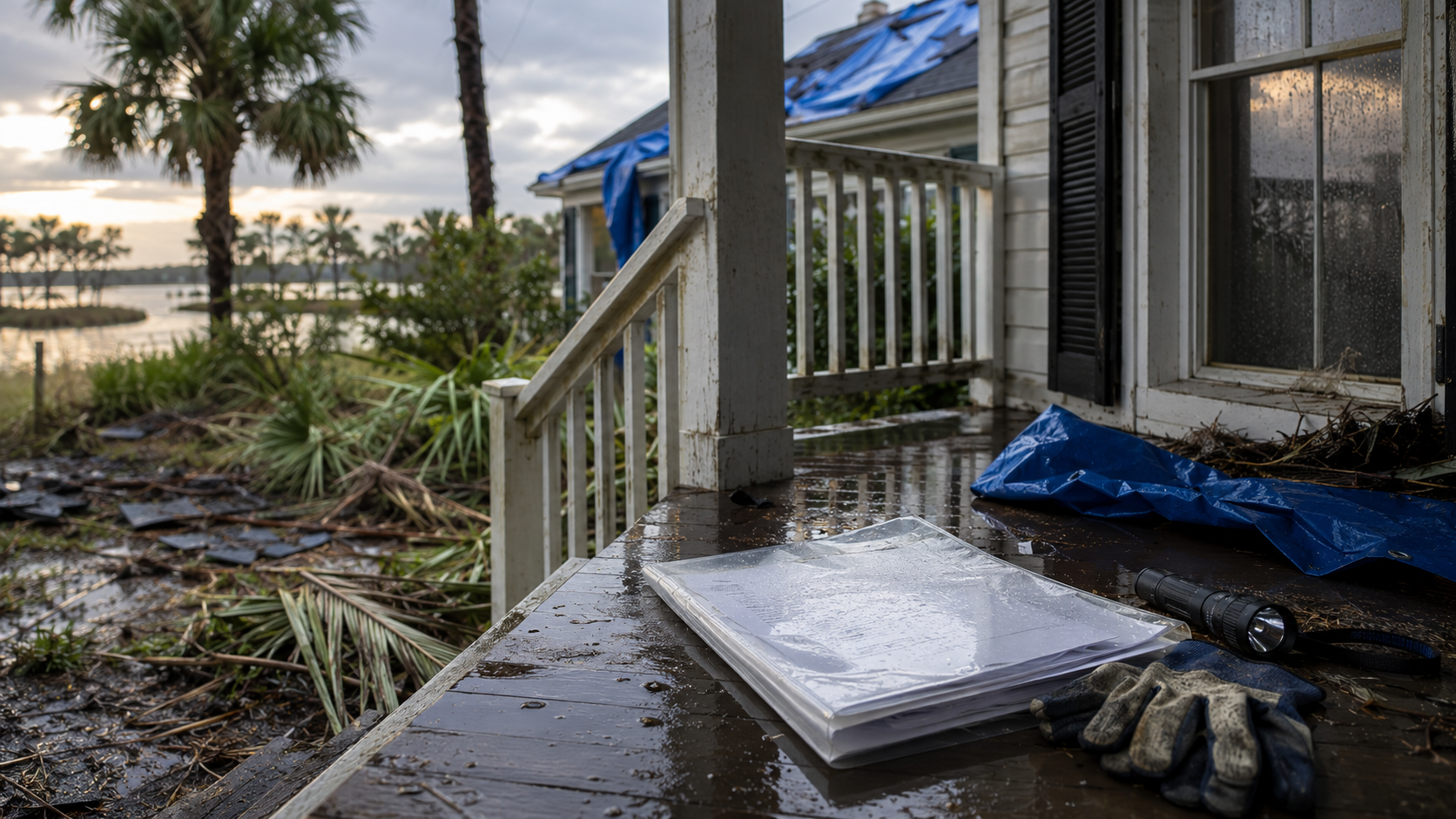

In early August 2024, Hurricane Debby moved into South Carolina after first striking Florida's Big Bend as a Category 1 hurricane. By the time it reached the South Carolina coast — making a second U.S. landfall near Bulls Bay — it had weakened to a tropical storm, but its slow, stalling track turned it into a prolonged rainfall event rather than a wind event. Charleston and the Lowcountry saw historic rainfall and widespread urban flooding, the state declared an emergency, river flooding became a serious concern inland in the Pee Dee, and tornadoes embedded in the outer bands damaged communities including Edisto Beach and the Moncks Corner area.

For property owners, a storm like Debby creates a particular kind of insurance problem. When most of the damage comes from water, the coverage outcome often turns on a single distinction that homeowners rarely think about until they need to: the difference between wind damage, which a standard homeowners policy generally covers, and flood damage, which it generally excludes. A claim that should be paid can be denied or underpaid because the carrier characterizes the loss as flood, or because a percentage hurricane deductible takes a large bite, or because the repair scope falls short of what the damage actually requires.

This guide walks through what Debby did across South Carolina, why wind-versus-flood causation is the central question on these claims, six considerations for SC property owners with a contested Debby claim, how the § 38-59-40 framework may apply, and how we at Property People Law approach contested SC storm claims. Every policy is different, every claim turns on its own facts.

What Hurricane Debby Did Across South Carolina

Debby's defining characteristic in South Carolina was water, not wind. After entering from Georgia, the storm slowed and lingered near the coast, drawing moisture off warm Atlantic waters and dropping extraordinary rainfall over the Charleston area and the surrounding Lowcountry. Streets across the Charleston peninsula and nearby communities flooded, the city imposed a rare curfew, and emergency crews conducted high-water rescues. Inland, river flooding became the dominant concern as the system moved through, with state officials shifting their response toward the Pee Dee region as rivers rose.

The storm also produced wind damage and tornadoes. Tornadoes embedded in Debby's outer bands struck communities including Edisto Beach and the Moncks Corner area, damaging homes and structures. So while the headline story was flooding, individual properties experienced a mix — wind and tornado damage at some addresses, water intrusion and flooding at others, and a combination at many. That mix is exactly what makes the coverage analysis on a Debby claim fact-specific: the same storm produced both generally-covered and generally-excluded perils, sometimes at the same property.

None of this changes the legal framework that governs a claim. South Carolina insurance law, the claim-handling regulations, and the § 38-59-40 framework apply to a Hurricane Debby claim the same way they apply to any SC property loss. What Debby changes is the factual battleground — because a slow, wet storm sharpens the wind-versus-flood question that decides so many of these claims.

Why Wind-Versus-Flood Causation Is the Central Question

A standard homeowners policy in South Carolina generally covers wind damage and wind-driven rain — for example, rain that enters after wind removes shingles or breaches the building envelope. It generally excludes flood, which includes rising surface water, storm surge, and the kind of widespread inundation that NFIP flood policies are designed to cover. After a storm like Debby, where water did much of the damage, the carrier's characterization of the loss often decides the claim: wind-driven water intrusion points toward coverage, while rising floodwater points toward the flood exclusion.

The difficulty is that the two can occur at the same property, and the sequence matters. If wind first opened the roof or a wall and rain then entered, that water intrusion may be covered even though it's water damage. If rising water entered at ground level independent of any wind damage, the flood exclusion generally applies. A careful claim documents what failed, when, and from what force — the storm sequence, the path the water took, and the type of damage at each location in the structure. A denial that broadly labels everything 'flood' without engaging that sequence is the most common dispute on these claims, and it isn't necessarily correct.

This is also why the anti-concurrent-causation clause in many policies matters on a Debby claim. That clause can affect how a loss is treated when a covered peril (wind) and an excluded peril (flood) combine to cause damage. How it applies depends on the specific policy language and the facts of the loss, and it's one of the provisions worth having reviewed closely when a storm involved both wind and water. Our SC anti-concurrent-causation guide covers that analysis.

What SC Homeowners Policies Generally Provide After a Storm Like Debby

Most SC homeowners policies are written on an HO-3-style form, covering the dwelling and other structures on an open-peril basis subject to exclusions, with personal property typically on a named-peril basis. Wind and wind-driven rain are generally covered perils; flood is generally excluded and requires a separate NFIP or private flood policy. Additional living expenses are usually covered when a covered peril makes the home uninhabitable — but if the displacement was caused by flood rather than a covered peril, that coverage may not apply.

Two terms deserve particular attention on a Debby-type claim. First, the hurricane or named-storm deductible: many SC coastal and wind-exposed policies carry a separate deductible for named-storm or hurricane damage, often a percentage of the dwelling limit rather than a flat dollar figure. Because Debby was a named storm, whether that deductible applies — and whether it was calculated correctly — can be a significant dollar question. Second, the roof settlement basis: roof coverage may be written on a replacement-cost or actual-cash-value basis depending on the roof's age and the policy terms, which affects how much the carrier owes before any recoverable depreciation.

As with any policy, resulting mold damage — a real risk after prolonged water exposure of the kind Debby produced — generally carries a sublimit, and the policy's notice and mitigation conditions apply. The specific language in your policy and on your declarations page controls. For a storm that happened in August 2024, gathering the policy in effect at the time, the declarations page, and the full claim file is the foundation for understanding what you were owed.

Six Considerations for SC Property Owners with a Contested Debby Claim

When a SC Hurricane Debby claim is contested, several considerations tend to drive how it resolves. None is unique to Debby — they're the same dispute categories that follow most SC storm losses — but a slow, wet storm brings them all into play at once.

- Pin down the wind-versus-flood characterization. This is the central question. Identify what damage came from wind or wind-driven rain (generally covered) versus rising water or storm surge (generally excluded), and document the sequence — what failed first, and how the water entered. A denial that labels the whole loss 'flood' without engaging that sequence is the most common Debby dispute, and the documentation of the storm's progression at your property is what supports the covered characterization.

- Check how the hurricane or named-storm deductible was applied. Because Debby was a named storm, confirm whether a percentage hurricane or named-storm deductible was applied, whether it was calculated correctly against the dwelling limit, and whether the policy's trigger for that deductible was actually met. On a high dwelling limit, the difference between a percentage deductible and a standard flat deductible can be thousands of dollars.

- Examine the roof scope and depreciation. Wind and any tornado activity from Debby produced roof damage at many properties. Roof claims frequently turn on whether the carrier's scope matches an independent roofer's assessment and whether depreciation was reasonable. On an actual-cash-value roof settlement, recoverable depreciation may be available once repairs are completed and documented. Compare the carrier's scope against an independent estimate before accepting it.

- Raise matching where only part of a structure is repaired. When a storm damages part of a roof or one elevation, the matching question arises: can the carrier repair only part when the replacement materials won't reasonably match the existing ones? Most SC policies require repairs of like kind and quality, which may support expanded scope when partial repair would leave a visibly mismatched result.

- Account for resulting mold and additional living expenses. Prolonged water exposure of the kind Debby caused can lead to mold, which generally carries a policy sublimit, and may make a home temporarily uninhabitable. If the displacement and any mold resulted from a covered peril rather than from flood, additional living expense and mold coverage may apply, subject to the policy's limits. Documenting the cause and the timeline matters for both.

- Gather the right records, even well after the storm. For a 2024 storm, pull the policy and declarations page in effect at the time, the full claim file, any engineering or adjuster report the carrier relied on, dated photos, and any independent contractor estimates. A reopened or supplemented claim is often built on documentation that shows the carrier's original scope or causation call didn't match the actual damage.

How the South Carolina § 38-59-40 Framework May Apply

Most contested Debby claims are ordinary coverage or scope disputes — the carrier reached one conclusion about causation or repair cost, the policyholder disagrees, and the evidence decides which position holds. That's the normal terrain of a storm claim and doesn't by itself implicate any bad-faith framework. A genuinely debatable wind-versus-flood question, handled in good faith, is the kind of dispute that gets resolved on the facts.

Where the analysis may move toward South Carolina's statutory framework is when the carrier refuses to pay a covered claim without reasonable cause. S.C. Code § 38-59-40 may allow a court to award attorney's fees — capped at one-third of the judgment and set within a reasonableness standard, not automatic and not the policyholder's full fees — in addition to the underlying policy benefit. The common-law bad-faith claim recognized in SC since the Tyger River line of cases may add consequential and potentially punitive damages when the carrier's conduct meets the bad-faith standard.

Whether either framework applies to a specific Debby claim depends on the carrier's actual conduct and what the record shows about the basis for the refusal. Labeling an entire loss 'flood' with little investigation, ignoring a documented wind-first sequence, or refusing to engage an independent contractor's scope are the kinds of conduct that can move a claim from ordinary dispute toward the statutory framework. A debatable question handled in good faith generally won't; a covered claim refused without reasonable cause may. See our SC bad-faith pillar for the full framework.

How Property People Law Approaches Contested SC Storm Claims

When a SC property owner reaches out about a denied or underpaid Hurricane Debby claim, the first conversation is free and the framework is consistent. We read the policy and the declarations page in effect at the time of the storm — the wind and wind-driven-rain coverage, the flood exclusion, the anti-concurrent-causation clause, the hurricane or named-storm deductible, the roof-settlement basis, the mold sublimit, and the notice and mitigation conditions. We pull the claim file and any engineering or adjuster report the carrier's position relied on.

From there we compare the carrier's position against the physical evidence, an independent contractor's scope, and the documented storm sequence at the property. We identify where the covered wind-versus-flood characterization is supportable, whether the deductible was applied correctly, where matching and recoverable depreciation add to the claim, whether mold and additional living expense were properly addressed, and whether the carrier's conduct may support a § 38-59-40 attorney-fee argument or the common-law bad-faith analysis. We work alongside SC property owners across every step of those disputes.

Our SC residential and commercial property work is generally on contingency — we only get paid from the recovery, not your pocket. Past results in other cases don't guarantee outcomes in any new matter, and every claim turns on its own facts.