- Potential Tropical Cyclone Eight struck southeastern North Carolina in mid-September 2024, dropping extreme rainfall — in places 15 to 20 inches — on the Carolina coast around Carolina Beach, Wilmington, and Brunswick County, causing major flash flooding even though it never strengthened into a named tropical storm.

- Because the system was never named, the central insurance question on many of these claims is the deductible: a hurricane or named-storm deductible generally should not apply to a storm that never became a named tropical system, which can make a significant dollar difference.

- As with any heavy-rain storm, wind and wind-driven rain are generally covered under a homeowners policy, while rising surface water and flash flooding are generally excluded and covered only under separate flood insurance — so wind-versus-flood causation still matters.

- When a NC carrier handles a claim unfairly — including by misapplying a hurricane deductible — N.C. Gen. Stat. § 75-1.1 may allow treble damages and attorney's fees, with § 58-63-15 setting the unfair-claim-settlement standards.

- At Property People Law, we review NC PTC Eight claims and any denial at no cost. Our NC residential and commercial property work is generally on contingency — we only get paid from the recovery, not your pocket.

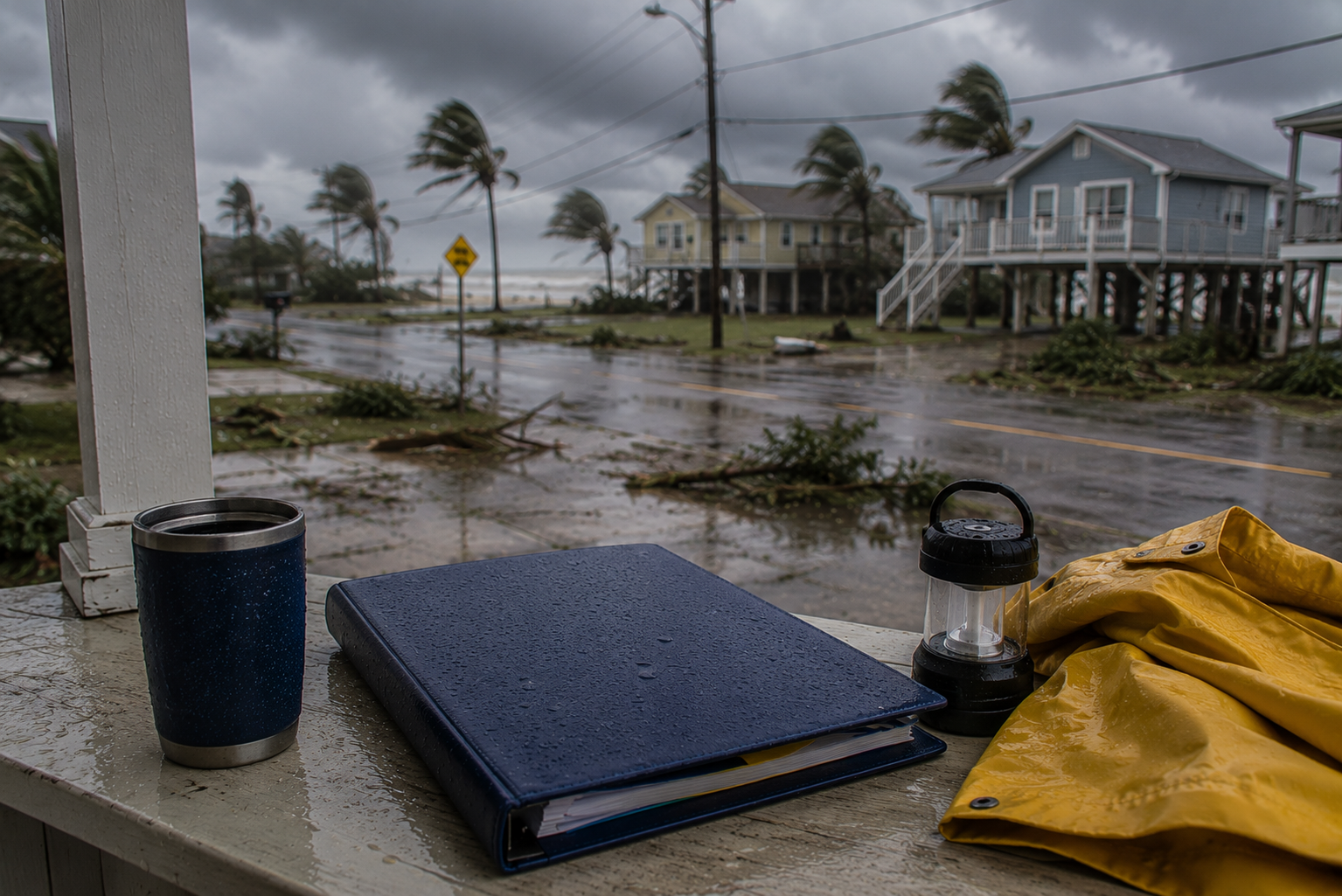

In mid-September 2024, a disorganized but extraordinarily wet system designated Potential Tropical Cyclone Eight stalled over southeastern North Carolina. It never strengthened into a named tropical storm — it remained a 'potential tropical cyclone,' the National Hurricane Center's designation for a system that threatens land but hasn't met the criteria for naming. Yet it dropped staggering rainfall on the Carolina coast: parts of the Carolina Beach, Wilmington, and Brunswick County area recorded 15 to 20 inches, triggering major flash flooding, water rescues, and a state of emergency in some communities.

For property owners, this storm created an unusual and specific insurance question. Because the system was never named, the hurricane or named-storm deductible that many coastal NC policies carry may not properly apply — and yet some carriers applied it anyway. That single issue can mean thousands of dollars. Layered on top is the familiar wind-versus-flood question that follows any heavy-rain event, where covered wind-driven water and excluded flooding have to be separated.

This guide walks through what PTC Eight did across North Carolina, why an unnamed storm may mean the hurricane deductible doesn't apply, the disputes that commonly arise, how the § 75-1.1 framework may apply, and how we at Property People Law approach contested NC storm claims. Every policy is different, every claim turns on its own facts.

What Potential Tropical Cyclone Eight Did Across North Carolina

The defining characteristic of PTC Eight was rainfall, not wind or naming status. The system stalled near the southeastern NC coast and trained heavy rain bands over the same areas for hours. The Carolina Beach, Wilmington, and Brunswick County area bore the brunt, with rainfall totals in the 15-to-20-inch range in the hardest-hit spots. Streets became rivers, neighborhoods flooded, water rescues were carried out, and some communities declared local states of emergency. The damage was overwhelmingly water-driven flash flooding.

Critically, the system never became a named tropical storm. It stayed classified as a potential tropical cyclone — a designation the National Hurricane Center uses to issue warnings for a system that may threaten land but hasn't organized enough to be named. That naming distinction, which might seem like a technicality, turns out to matter a great deal for insurance, because the trigger for many hurricane and named-storm deductibles is tied specifically to a named system.

None of this changes the legal framework that governs a claim. North Carolina insurance law, the § 58-63-15 unfair-claim-settlement standards, and the § 75-1.1 unfair-trade-practices framework apply to a PTC Eight claim the same way they apply to any NC property loss. What PTC Eight changes is the factual battleground — because an unnamed, rain-driven storm raises both a deductible-trigger question and the wind-versus-flood question.

Why an Unnamed Storm May Mean the Hurricane Deductible Doesn't Apply

Many coastal NC homeowners policies carry a separate hurricane or named-storm deductible — often a percentage of the dwelling limit rather than a flat dollar amount — that applies to damage from a hurricane or named tropical storm. The key is the trigger language. These deductibles are typically triggered by a system that the National Hurricane Center has named, or that has reached hurricane or named-storm status, sometimes within defined dates tied to the storm.

Potential Tropical Cyclone Eight was never named. It never became Tropical Storm or Hurricane anything. So for many policies, the precise trigger for the hurricane or named-storm deductible was arguably never met — which would mean the standard (and usually much lower) all-other-perils deductible should apply instead. On a percentage deductible against a substantial dwelling limit, the difference between the two can be many thousands of dollars out of the property owner's pocket.

This is why the first thing worth checking on a PTC Eight claim is which deductible the carrier applied and what the policy's trigger language actually says. If a carrier applied a percentage hurricane deductible to damage from a storm that never met the naming trigger, that may be incorrect, and correcting it can substantially increase the net recovery. The answer turns entirely on the specific trigger wording in your policy — which is exactly the kind of provision worth having read closely.

What NC Homeowners Policies Generally Provide After a Storm Like PTC Eight

Most NC homeowners policies are written on an HO-3-style form, covering the dwelling and other structures on an open-peril basis subject to exclusions, with personal property typically on a named-peril basis. Wind and wind-driven rain are generally covered perils; flood, including flash flooding and rising surface water, is generally excluded and requires a separate NFIP or private flood policy. Additional living expenses are usually covered when a covered peril makes the home uninhabitable — but if the displacement was caused by flood rather than a covered peril, that coverage may not apply.

The standout issue on a PTC Eight claim is the deductible, as described above — but the roof and water-intrusion provisions matter too. Roof coverage may be written on a replacement-cost or actual-cash-value basis depending on the roof's age and the policy terms, and how wind-driven rain intrusion is treated depends on the specific policy language regarding openings created by a covered peril.

As with any policy, resulting mold — which can follow wind-driven rain intrusion if it isn't dried out promptly — generally carries a sublimit, and the policy's notice and mitigation conditions apply. The specific language in your policy and on your declarations page controls. For a storm in September 2024, gathering the policy in effect at the time, the declarations page, and the full claim file is the foundation for understanding both the deductible question and what you were owed.

The Disputes That Commonly Arise on PTC Eight Claims

When a NC PTC Eight claim is contested, several disputes tend to drive how it resolves. The deductible question is distinctive to an unnamed storm; the others are the familiar categories that follow most NC water-driven storm losses.

- The hurricane-deductible question. This is the distinctive PTC Eight issue. Confirm which deductible the carrier applied and compare it against the policy's trigger language. Because the system was never named, a percentage hurricane or named-storm deductible may not properly apply — and correcting that can mean thousands of dollars back to the property owner.

- The wind-versus-flood characterization. Identify what damage came from wind or wind-driven rain (generally covered) versus flash flooding and rising surface water (generally excluded), and document the sequence. A denial that labels the whole loss 'flood' without engaging that sequence is a common dispute, and documentation of how the water entered is what supports the covered characterization.

- Wind-driven rain intrusion. Where wind created an opening in the roof or building envelope and rain then entered, that intrusion is generally covered. The carrier may try to treat all interior water as excluded flood; separating wind-driven intrusion from rising water is what supports the claim.

- Roof scope and depreciation. Roof claims turn on whether the carrier's scope matches an independent roofer's assessment and whether depreciation was reasonable. On an actual-cash-value roof settlement, recoverable depreciation may be available once repairs are completed and documented.

- Matching where only part of a structure is repaired. While North Carolina has no specific matching statute, most policies' like-kind-and-quality language may support expanded scope when partial repair would leave a visibly mismatched result. Our NC matching guide covers how to argue it under the policy.

- Gathering the right records. Pull the policy and declarations page in effect at the time, the full claim file, any report the carrier relied on, dated photos, and any independent contractor estimates. A reopened or supplemented claim — or a corrected deductible — is often built on documentation that shows the carrier's original position didn't match the policy or the damage.

How North Carolina's § 75-1.1 and Unfair-Claims Framework May Apply

Most contested claims from this storm are ordinary coverage, scope, or deductible disputes — the carrier reached one conclusion, the policyholder disagrees, and the evidence and the policy language decide which position holds. That's the normal terrain of a storm claim and doesn't by itself implicate any statutory penalty framework. A genuine disagreement over roof scope, or a deductible applied on a defensible reading of the policy, handled in good faith, gets resolved on the facts.

North Carolina's framework for insurer misconduct runs through two statutes. N.C. Gen. Stat. § 58-63-15 defines unfair claim settlement practices — the claim-handling conduct insurers are required to avoid. And N.C. Gen. Stat. § 75-1.1, the Unfair and Deceptive Trade Practices Act, may provide a remedy of treble damages and attorney's fees when an insurer's conduct is found to be an unfair or deceptive practice. A November 2024 bulletin from the North Carolina Insurance Commissioner addressed claim-handling expectations following that year's storms; we reference it as neutral context for the standards carriers are expected to meet, not as a comment on any particular claim.

Whether that framework applies to a specific Potential Tropical Cyclone Eight claim depends entirely on the carrier's actual conduct. Applying a hurricane deductible to an unnamed storm with no basis in the policy's trigger language, refusing to engage a documented independent estimate of wind and roof damage, or ignoring evidence are the kinds of conduct that can move a claim from ordinary dispute toward the statutory framework. A debatable position taken in good faith generally won't. See our NC bad-faith pillar for the full framework.

How Property People Law Approaches Contested NC Storm Claims

When a NC property owner reaches out about a denied or underpaid Potential Tropical Cyclone Eight claim, the first conversation is free and the framework is consistent. We read the policy and the declarations page in effect at the time of the storm — and we look first at the deductible, checking whether a hurricane or named-storm deductible was applied and whether this unnamed system actually met the policy's trigger. We then review the wind and wind-driven-rain coverage, the roof-settlement basis, the anti-concurrent-causation clause, the mold sublimit, and the notice and mitigation conditions. We pull the claim file and any report the carrier's position relied on.

From there we compare the carrier's position against the physical evidence and an independent contractor's scope. We identify whether the deductible was correctly applied, where the carrier's estimate falls short of the actual wind and roof damage, whether wind-driven-rain intrusion was properly accounted for, where matching and recoverable depreciation add to the claim, and whether the carrier's conduct may support a § 75-1.1 argument alongside the § 58-63-15 standards. We work alongside NC property owners across every step of those disputes.

Our NC residential and commercial property work is generally on contingency — we only get paid from the recovery, not your pocket. Past results in other cases don't guarantee outcomes in any new matter, and every claim turns on its own facts.