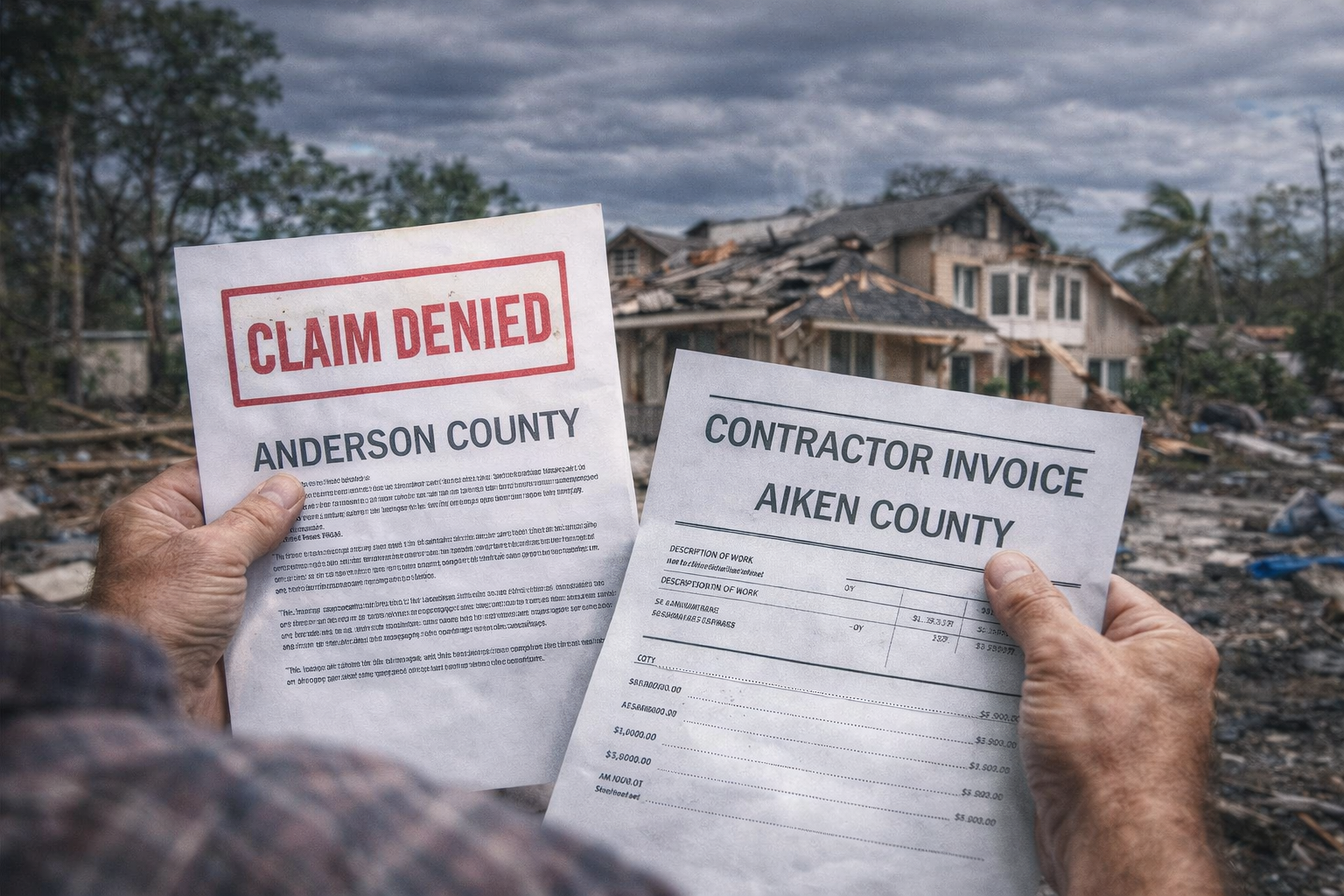

Hurricane Helene didn’t spare Anderson or Aiken. When the storm pushed through the South Carolina Upstate and western Midlands in late September 2024, it brought hurricane-force wind gusts, torrential rain, downed trees, and widespread power outages to two communities that rarely see this level of destruction. Both Anderson County and Aiken County were included in the federal disaster declaration, with FEMA providing individual assistance to affected residents.

In the months since, many homeowners in Anderson and Aiken have discovered that the damage to their properties was worse than they initially thought and that their insurance companies paid far less than the actual cost of repairs. If that sounds familiar, you have options.

Anderson County took a direct hit from Helene’s inland wind corridor. The storm produced sustained winds and gusts that toppled mature trees across residential neighborhoods in Anderson, Belton, Williamston, and Pendleton. Roof damage was widespread, with wind-driven debris and lifted shingles reported across the county. Flooding along creeks and low-lying areas caused water intrusion in homes that had never experienced flooding before. Power outages lasted for days, and the cascading effects spoiled food, sump pump failures, lack of climate control leading to moisture build up, compounded the property damage well beyond what was immediately visible.

Aiken County experienced significant tree damage across residential areas, parks, and rural properties. The SC Department of Insurance held a dedicated Insurance Claims Village in Aiken in early October 2024, with representatives from State Farm, USAA, Allstate, Travelers, and other major carriers on site to help residents file claims. That level of response underscores the severity of the damage. Neighborhoods in Aiken, North Augusta, and the surrounding areas reported roof damage, structural damage from fallen trees, water intrusion, and prolonged power outages. The Aiken area’s older housing stock with mature trees close to homes, made properties particularly vulnerable to wind and debris damage.

Insurance adjusters deployed to Anderson and Aiken after Helene frequently relied on national pricing databases that underestimate what it actually costs to hire a licensed contractor in these markets. Post-storm demand for roofers, general contractors, and restoration specialists drove up labor and material costs across the region. If your insurer’s estimate came in significantly below what local contractors are quoting, that gap represents money you may be owed.

Tree damage was the defining feature of Helene’s impact across Anderson and Aiken. Homeowners policies generally cover damage that a fallen tree causes to the home or other covered structures but insurers frequently dispute the scope of that coverage. Common disputes include: whether the insurer will pay for full tree removal versus only the portion on the structure, whether structural damage caused by the tree’s impact extends beyond the obvious contact point, and whether secondary damage from the tree’s impact (water intrusion through a compromised roof, for example) is included in the claim.

Both Anderson and Aiken have significant numbers of older homes with aging roofs and established landscaping. Insurers operating in these markets have been aggressive about attributing Helene damage to pre-existing wear, aging materials, or deferred maintenance. If your insurer told you that your roof damage was caused by “age” rather than the storm, that determination is worth challenging particularly with an independent contractor inspection and, if necessary, an engineering assessment.

Many Anderson and Aiken homeowners received notice that their damage fell below their hurricane or wind/hail deductible resulting in no payout. These percentage-based deductibles can be substantial: 2% on a $300,000 home means $6,000 out of pocket before the insurer pays anything. If the insurer’s damage estimate conveniently falls just below that threshold, an independent assessment may reveal the true cost exceeds the deductible and triggers a payout the insurer should have made.

1. Document all remaining damage. Photograph and video everything. Save all correspondence with your insurer, all contractor estimates, and all receipts for out-of-pocket expenses.

2. Get a local contractor estimate. Hire a licensed contractor who works in the Anderson or Aiken market and understands local labor rates, material costs, and building code requirements. Their estimate is your strongest evidence in a dispute.

3. Review your policy and deductible. Check your declarations page to understand what deductible was applied, what coverage you purchased, and whether your insurer’s payout aligns with the policy terms.

4. Don’t sign a release. If your insurer asks youto sign any document in exchange for a payment, have an attorney review it first.

5. Contact a property damage attorney. The Property People Law represents homeowners across Anderson County, Aiken County, and the surrounding communities. We offer free case evaluations and handle hurricane claim disputes on contingency, you pay nothing unless we recover additional compensation for you.

Hurricane Helene hit these communities hard. If your insurance company didn’t hold up their end of the deal, The Property People Law is here to fight for the compensation your policy provides. Contact us today for a free, no-obligation case evaluation.